Cerebras Systems, the AI chipmaker behind the world’s largest computer chip, saw its stock drop roughly 10% on its second day of public trading, closing near $280 on May 15, 2026. The pullback followed a first-day surge that carried shares to an intraday high of approximately $385, according to market data, before they settled around $311 at the close for a gain of about 68% over the $185 offering price.

Even after the retreat, CBRS sat about 51% above its IPO level. For investors watching from the sidelines, the two-day swing posed a straightforward question: does the premium reflect genuine demand for Cerebras’s technology, or the kind of speculative froth that tends to burn off once the novelty fades?

How Cerebras reached the public markets

Cerebras sold 30,000,000 shares at $185 each on the Nasdaq Global Select Market under the ticker CBRS, according to its final prospectus filed with the SEC. The base deal raised approximately $5.55 billion in gross proceeds, placing it among the largest U.S. technology IPOs in recent memory. The offering was led by a syndicate that included major Wall Street banks, as detailed in the prospectus.

The SEC declared the registration statement effective at 4:00 p.m. on May 13, 2026, per the agency’s effectiveness notice, clearing the last regulatory gate before shares could begin trading the next morning.

The road to that moment was anything but smooth. Cerebras originally filed for an IPO in late 2024 but hit delays linked to U.S. government scrutiny of its commercial relationship with G42, the Abu Dhabi-based technology group and one of its largest customers. The Commerce Department and national security officials examined whether Cerebras’s chip sales to G42 raised export-control concerns, given the geopolitical sensitivity surrounding advanced AI hardware. By the time the offering launched in May 2026, the company had secured the necessary regulatory clearances, though the prospectus continued to flag customer concentration as a material risk.

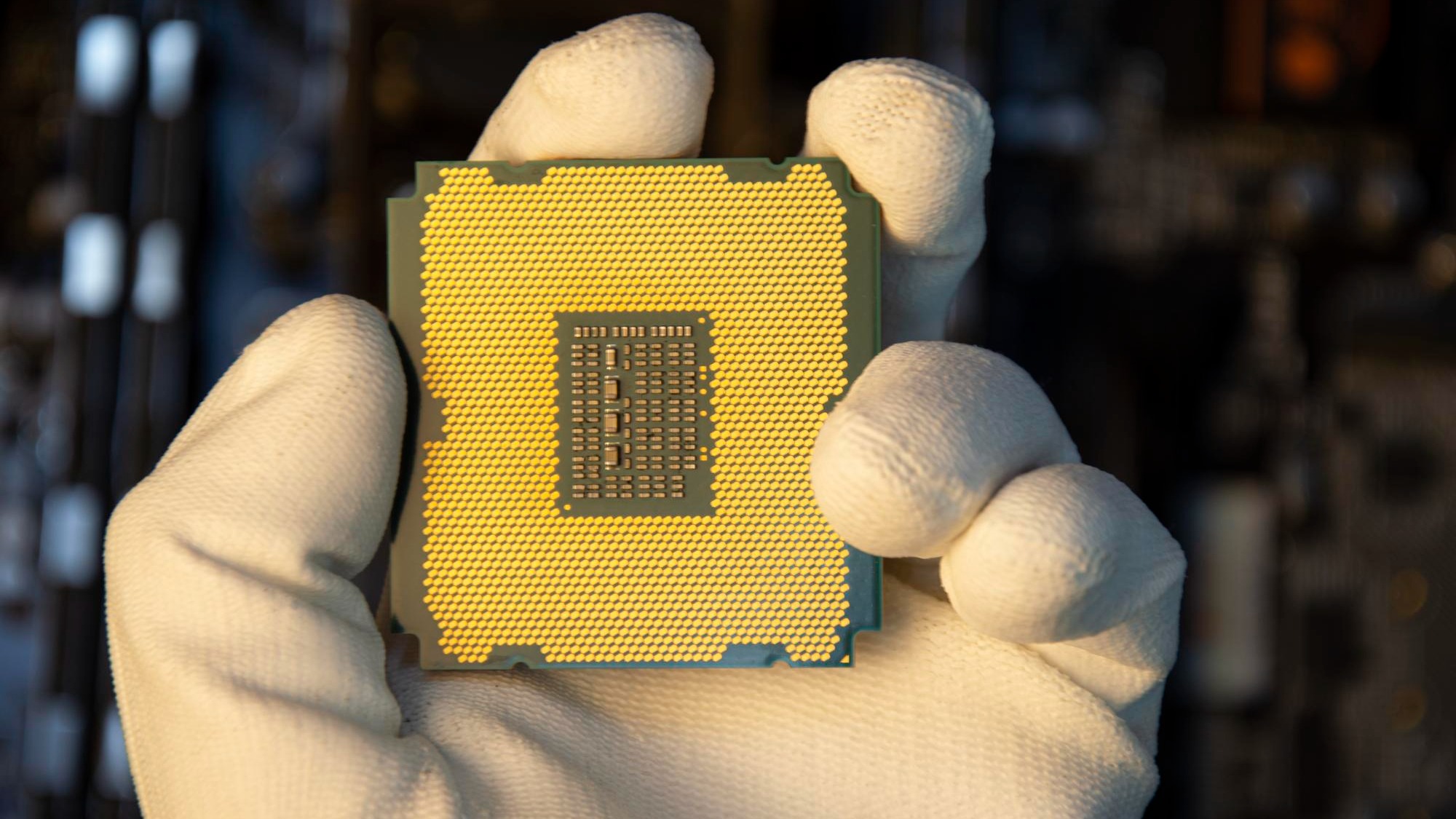

What Cerebras actually builds

Cerebras is not a conventional chipmaker. Its flagship product, the Wafer Scale Engine (WSE), occupies an entire semiconductor wafer, a single silicon chip roughly 100 times larger than Nvidia’s biggest GPUs. The logic behind the design is straightforward even if the engineering is extraordinarily difficult: by keeping everything on one massive die, Cerebras eliminates the communication bottlenecks that plague systems stitched together from clusters of smaller chips.

That architecture targets the same workloads fueling explosive demand for Nvidia’s H100 and B200 GPUs: training and running large AI models. Cerebras sells complete systems built around the WSE and has also begun offering cloud-based inference services. The company claims its hardware can train certain AI models dramatically faster than GPU-based alternatives, though independent, peer-reviewed benchmarks comparing the two at equivalent scale remain limited.

The competitive landscape is formidable. Nvidia controls the bulk of the AI accelerator market and benefits from CUDA, the software platform most AI researchers already rely on. AMD, Intel, and custom silicon programs at Google, Amazon, and Microsoft are all pursuing the same opportunity with deep pockets and established customer relationships. Cerebras, which disclosed in its prospectus that G42 alone accounted for a majority of its revenue in recent fiscal periods, must demonstrate it can win meaningful, recurring revenue against those incumbents rather than relying on a small number of headline-grabbing deals.

What the prospectus reveals about the business

The prospectus offers the clearest window into where Cerebras stands financially. The company reported revenue of approximately $136 million for the fiscal year ended March 2025, up sharply from roughly $79 million the prior year, according to the filing. Over the same period, Cerebras disclosed a net loss of approximately $867 million, widening from about $127 million a year earlier, reflecting heavy spending on research, manufacturing ramp-up, and stock-based compensation. Revenue has been concentrated among a small number of customers, with G42 accounting for a substantial share, a dependency the company itself identifies as a key risk factor.

At a closing price of $280, new buyers are paying a 51% premium over the price that IPO allocators locked in just two days earlier. That premium embeds real expectations: that Cerebras will diversify its customer base, that its technology will hold up against Nvidia’s rapidly advancing product roadmap, and that revenue growth will be steep enough to justify a valuation in the tens of billions of dollars.

D.A. Davidson analyst Gil Luria, who covers the semiconductor sector, noted in a May 2026 research brief that Cerebras’s IPO valuation “prices in years of flawless execution” and that the stock’s trajectory will depend on whether the company can convert its technological differentiation into a broadening book of recurring contracts.

What the day-two selloff actually tells us

A 10% decline on the second trading day, while sharp in dollar terms, is a well-documented pattern for IPOs that spike at the open. Investors who received shares at $185 were sitting on enormous paper gains within hours. For institutional holders and hedge funds, trimming that kind of windfall is standard portfolio management, not necessarily a verdict on the company’s prospects.

Detailed data on who sold and in what volume has not been published, so it is impossible to pinpoint how much of the selling came from institutional flippers versus retail traders taking profits. What the price action does reveal is that buyers on day two were unwilling to pay anywhere near the debut-session highs once the initial rush for exposure subsided.

Lock-up agreements described in the prospectus restrict most insiders and pre-IPO investors from selling their shares for 180 days following the offering, as specified in the filing’s lock-up provisions. That means the current float is relatively thin, consisting primarily of the 30 million IPO shares plus any additional stock released through the underwriters’ overallotment option. A small float can amplify moves in both directions, making these early sessions a poor predictor of where the stock will settle once the full shareholder base is free to trade.

Cerebras management has not commented publicly on the stock’s early swings, which is typical. Companies face restrictions on promotional statements around the time of an offering, and executives rarely benefit from reacting to price moves they cannot control.

Why Cerebras’s next quarterly filing will matter more than its first week of trading

In the near term, CBRS will likely be driven by sentiment, technical trading dynamics, and any fresh contract announcements. Over the next several quarters, though, the focus will shift to execution. Can Cerebras broaden its customer base beyond a handful of large buyers? Can it grow revenue while narrowing losses? Can it defend its technological edge as Nvidia, AMD, and the hyperscalers pour billions into competing chip designs?

The first two days of trading delivered plenty of drama. Answering those questions will take considerably longer, and the answers will determine whether Cerebras becomes a durable force in AI hardware or remains a spectacular IPO story that peaked early.